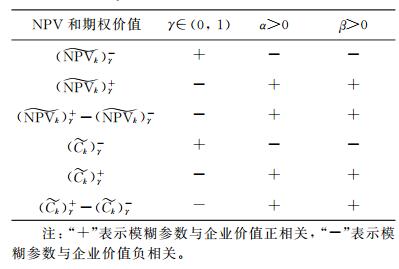

Abstract:Key parameter interval changes are used to quantify start-ups uncertainty and to deduce the discounted cash flow (DCF) and a compound real options model based on fuzzy theory. This research shows that the fuzzy real option method improves the DCF by giving the range of values with a fuzzy uncertainty to make more reasonable valuations. The fuzzy parameter sensitivity analysis shows that the start-ups uncertainty negatively correlates with the probability, the minimum value positively correlates with the left width, and the maximum value positively correlates with the right width. Analyses of the start-ups values for different situations can improve the investment decision accuracy. A case study further verifies the effectiveness of the fuzzy real options method in multi-stage investments for start-ups.

[1] BLACK F S, SCHOLES M S. The pricing of options and corporate liabilities[J]. Journal of Political Economy, 1973, 81(3):637-654. [2] MYERS S C. Determinants of corporate borrowing[J]. Journal of Financial Economics, 1977, 5(2):147-175. [3] 郑征, 朱武祥. 运用复合实物期权方法研究初创企业的估值[J]. 投资研究, 2017, 36(4):118-135. ZHENG Z, ZHU W X. Application of compound real options method in the start-ups valuation[J]. Review of Investment Studies, 2017, 36(4):118-135. (in Chinese) [4] ZADEH L A. Fuzzy sets[J]. Information and Control, 1965, 8(3):338-353. [5] BUCKLEY J J. The fuzzy mathematics of finance[J]. Fuzzy Sets and Systems, 1987, 21(3):257-273. [6] CARLSSON C, FULLÉR R. A fuzzy approach to real option valuation[J]. Fuzzy Sets and Systems, 2003, 139(2):297-312. [7] YOSHIDA Y. A discrete-time model of American put option in an uncertain environment[J]. European Journal of Operational Research, 2003, 151(1):153-166. [8] WU H C. Pricing European options based on the fuzzy pattern of Black-Scholes formula[J]. Computers & Operations Research, 2004, 31(7):1069-1081. [9] WU H C. Using fuzzy sets theory and Black-Scholes formula to generate pricing boundaries of European options[J]. Applied Mathematics and Computation, 2007, 185(1):136-146. [10] XU W J, PENG X L, XIAO W L. The fuzzy jump-diffusion model to pricing European vulnerable options[J]. International Journal of Fuzzy Systems, 2013, 15(3):317-325. [11] WANG X D, HE J M, LI S W. Compound option pricing under fuzzy environment[J]. Journal of Applied Mathematics, 2014:875319. [12] TAVAKKOLNIA A. A binomial tree valuation approach for compound real options with fuzzy phase-specific volatility[C]//Proceedings of the 12th International Conference on Industrial Engineering. Tehran, Iran, 2016:73-78. [13] BI X, WANG X F. The application of fuzzy-real option theory in BOT project investment decision-making[C]//Proceedings of the 16th International Conference on Industrial Engineering and Engineering Management. Beijing, China, 2009:289-293. [14] PUSHKAR S, MISHRA A. IT project selection model using real option optimization with fuzzy set approach[M]//ARIWA E, EL-QAWASMEH. Digital enterprise and information systems. Berlin, Germany:Springer, 2011, 194:116-128. [15] WANG Q, KILGOUR D M, HIPEL K W. Facilitating risky project negotiation:An integrated approach using fuzzy real options, multicriteria analysis, and conflict analysis[J]. Information Sciences, 2015, 295:544-557. [16] BIANCARDI M, VILLANI G. Robust Monte Carlo method for R&D real options valuation[J]. Computational Economics, 2017, 49(3):481-498. [17] DE ANDRÉS-SÁNCHEZ J. An empirical assestment of fuzzy Black and Scholes pricing option model in Spanish stock option market[J]. Journal of Intelligent & Fuzzy Systems, 2017, 33(4):2509-2521. [18] ZMEŠKAL Z. Application of the fuzzy-stochastic methodology to appraising the firm value as a European call option[J]. European Journal of Operational Research, 2001, 135(2):303-310. [19] YAO J S, CHEN M S, LIN H W. Valuation by using a fuzzy discounted cash flow model[J]. Expert Systems with Applications, 2005, 28(2):209-222. [20] WANG J, HWANG W L. A fuzzy set approach for R&D portfolio selection using a real options valuation model[J]. Omega, 2007, 35(3):247-257. [21] SEMERCIOGLU N, TOLGA A Ç. A multi-stage new product development using fuzzy type-2 sets in a real option valuation[C]//Proceedings of 2015 IEEE International Conference on Fuzzy Systems. Istanbul, Turkey, 2015:1-7. [22] 赵振武, 唐万生. 模糊实物期权理论在风险投资项目价值评价中的应用[J]. 北京理工大学学报(社会科学版), 2006, 8(1):49-51. ZHAO Z W, TANG W S. The application of fuzzy real option theory in the venture investment value evaluation[J]. Journal of Beijing Institute of Technology (Social Sciences Edition), 2006, 8(1):49-51. (in Chinese) [23] 张维功, 何建敏, 吕宏生. 基于B-S公式的模糊实物期权研究[J]. 统计与决策, 2009(3):143-145. ZHANG W G, HE J M, LÜ H S. Research on fuzzy real option based on B-S formula[J]. Statistics and Decision, 2009(3):143-145. (in Chinese) [24] 张茂军, 秦学志, 南江霞. 基于三角直觉模糊数的欧式期权二叉树定价模型[J]. 系统工程理论与实践, 2013, 33(1):34-40. ZHANG M J, QIN X Z, NAN J X. Binomial tree model of the European option pricing based on the triangular intuitionistic fuzzy numbers[J]. Systems Engineering:Theory & Practice, 2013, 33(1):34-40. (in Chinese) [25] 李双兵, 冀巨海. 高新技术企业风险投资价值评估:基于模糊实物期权视角[J]. 财会通讯, 2016(5):8-10. LI S B, JI J H. Value evaluation of venture capital in hi-tech enterprises:Based on fuzzy real option perspective[J]. Communication of Finance and Accounting, 2016(5):8-10. (in Chinese) [26] 赵昕, 薛岳梅, 丁黎黎. 灰色模糊环境下基于跳扩散过程的脆弱期权定价模型[J]. 系统工程, 2017, 35(12):35-42. ZHAO X, XUE Y M, DING L L. Vulnerable option pricing model based on jump-diffusion process for grey ambiguity condition[J]. Systems Engineering, 2017, 35(12):35-42. (in Chinese)

2019, Vol. 59

2019, Vol. 59